The Vision

Ideal Financial Freedom Setup

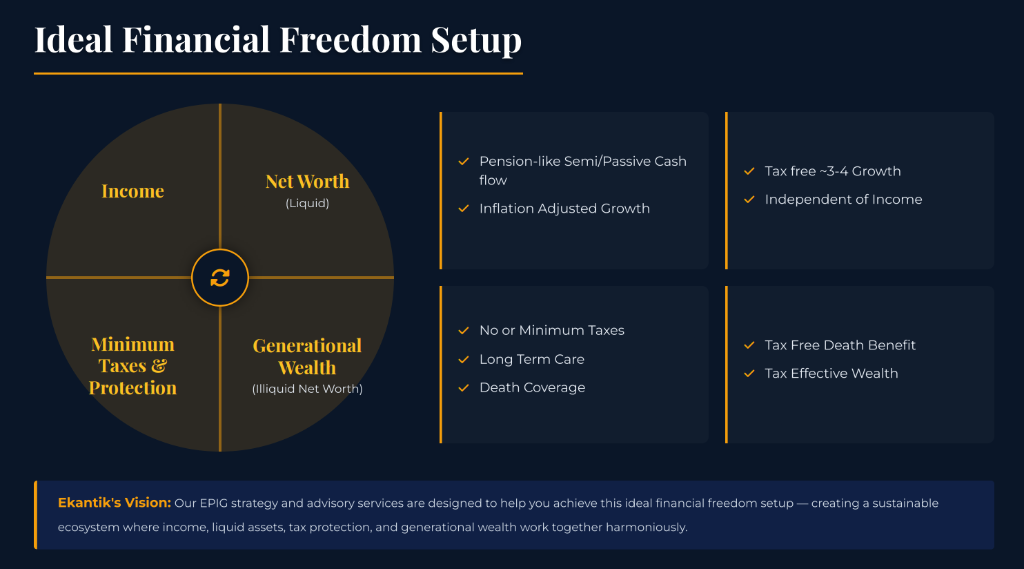

The four pillars of true financial independence—income, liquidity, coverage, and legacy.

EPIG 500 is a rules-based S&P 500 strategy for wealth preservation and tax-efficient growth toward your 10-year wealth goals: full participation in bull markets, 0% cash in down markets—growth without maximum risk.

Escape velocity: the capital at which your portfolio’s thrust clears the gravity of your expenses.

Support-rate archetypes (illustrative — each trades off liquidity, perpetuity, and scalability):

Capital required to fund the same income — the higher the (illustrative) support rate, the less capital, with different tradeoffs.

FCR ≥ 1.25 — income covering life with margin. That’s the page’s own published standard.

The four pillars of true financial independence—income, liquidity, coverage, and legacy.

The ECA wealth-building system is designed to achieve all four quadrants through a tax-efficient, income-generating cycle.

Our proprietary wealth-building cycle delivers Income, Liquidity, and Legacy outcomes.

Success requires understanding the universal path to freedom—and the mindset that makes it real.

A baseline you can maintain + extra deposits in strong months = a reservoir you can access without permanently draining your base.

This is why "save what's left" usually fails—as your income grows, lifestyle expenses creep up to consume the surplus. Willpower alone can't compete with this structural tendency.

Floor + Surge is a constraint-based system that reverses the equation: you commit to a baseline contribution first, then layer on additional deposits during strong cash-flow months. The system creates the discipline that motivation cannot sustain.

A fixed annual amount you can always fund, even in a rough year. This becomes your non-negotiable minimum—the foundation that compounds regardless of income volatility.

When cash flow grows—bonuses, business profits, windfalls, strong performance years—you layer on additional deposits. This captures upside without creating unsustainable obligations.

Over time, you build a reservoir that supports opportunities, absorbs emergencies, and provides retirement flexibility—all while your base continues to compound.

Traditional savings accounts are designed for accumulation—every withdrawal permanently shrinks the pile. You're always choosing between liquidity and growth.

A reservoir is different. It's engineered so that accessing liquidity can be treated as financing rather than permanent withdrawal. This means your base can keep compounding even when you need to tap it—though access has real costs and requires responsible management. You get both: growth potential and liquidity when opportunities or needs arise.

You want a system over motivation—structure that creates discipline automatically

You have income upside—variable comp, business profits, or growing earnings

You value liquidity + stability—want both access and compounding, not either/or

This is not a "hack" or loophole. Accessing your reservoir has real costs—interest, opportunity cost, and potential impact on long-term growth if not managed responsibly. Outcomes depend on proper design, ongoing maintenance, and disciplined use. This approach works best when engineered correctly and monitored regularly. Consult with qualified financial, tax, and legal professionals before implementing any wealth strategy.

How do you actually build this reservoir? With EPIG 500—designed to compound through bull markets while sidestepping the crashes.

A rules-based S&P 500 strategy that matches market performance in bull years and shifts to 0% cash in down markets—delivering outperformance through drawdown avoidance, not market timing.

Designed to participate fully with the S&P 500 in bull markets and shift to 0% cash in down markets—aiming to sidestep major drawdowns

Binary Risk ON/OFF "light switch" approach reacts to trend signals with discipline—no emotional decision-making, no market forecasting

0.5%–1% risk per trade framework keeps individual position losses small while targeting outsized gains in favorable conditions

Built on SPY and/or S&P 500 futures for efficient execution, transparency, and institutional-grade liquidity

Built and stress-tested against decades of market history—bull runs, sharp corrections, and extended flat "lost decade" periods—to pursue durable, all-weather compounding

Avoiding large drawdowns by moving to cash preserves capital and improves long-term compounding—because steep losses require outsized gains just to break even

Move the sliders — the math is yours to check.

Lose 30%, and you need 43% just to get back to even. The market doesn’t refund your time.

Volatility is a tax on compounding — this is arithmetic, not opinion. ($100,000 over 10 years.)

See the full strategy on the dedicated EPIG 500 site—portfolio allocation, the rules-based Risk ON/OFF system, the multi-cycle backtest, and the complete performance story versus the S&P 500.

Learn More About EPIG 500Targeted Outcomes, Not Promises. EPIG 500 targets full upside participation with 0% exposure in down markets, but these are goals—not guarantees. Actual results may underperform, and capital losses are possible. Any performance figures shown on the dedicated EPIG 500 site are backtested/hypothetical and do not predict future results.

Not Investment, Tax, or Legal Advice. This description is informational and educational only. It does not constitute investment advice, a recommendation, or an offer/solicitation. Consult qualified professionals before making decisions.

EPIG 500 compounds your long-term wealth engine by reducing the "volatility tax"—prioritizing drawdown defense to improve multi-decade compounding. It's the growth core of your founding member charter.

Every decision, every structure, every tool is guided by three core principles—designed to deliver freedom without fragility.

Layer multiple forms of leverage so each layer amplifies the next—creating upward compounding over time.

Let's verify this approach aligns with your wealth goals and timeline.

Each layer strengthens the one below it.

What would these approaches mean for your specific situation? Model your numbers, see your outcomes, understand your path forward.

You've learned how EPIG 500 is designed to grow your wealth forever. Now model your specific situation: your age, your capital, your timeline, your goals. See how different approaches create income, liquidity, and legacy outcomes tailored to your life.

Compare two paths: Direct investing (traditional) vs. Whole Life + EPIG borrowing (reservoir approach). Adjust every variable to match YOUR reality—then see which path aligns with your freedom goals.

Every number below can be adjusted. Start with the defaults to see an example, then customize to match your actual situation—your age, capital, income needs, and goals.

Invest full annual contribution directly in EPIG. Pay taxes at exit. Use 70/30 split for income vs liquidity.

Plan 1 Strategy:

• Invest 100% of annual contribution directly in EPIG

• Pay capital gains tax on profits when liquidating

• Split after-tax capital: 70% annuitized, 30% liquid fund

Pay annual premium to policy. Borrow specified % and invest in EPIG. Pay loan interest. Tax on liquidation.

Plan 2 Strategy:

• Pay annual premium to whole life policy (builds cash value)

• Borrow specified % from policy and invest in EPIG

• Pay interest on outstanding loan balance (from EPIG)

• Pay capital gains tax on EPIG profits when liquidating

• Same 70/30 income conversion as Plan 1: annuitize 70% of Net EPIG + draw tax-free policy loans against 70% of cash value; 30% of Net EPIG stays liquid

Click Calculate to see your results

Lock in lifetime benefits available only during our founding member period

Flat annual fee locked in forever — no matter how large your portfolio grows. Your rate is set today and locked against future increases.

Earn toward $0 annual fees forever. When you hit specific wealth goal milestones, your advisory fees can be eliminated permanently.

Complete Done-For-You Wealth Management: We execute the EPIG 500 strategy, handle ongoing optimization, provide quarterly portfolio reviews, and ensure tax-efficient wealth growth—all managed for you.

We act as your complete fiduciary partner, coaching you toward self-sufficiency. Success means you can eventually manage wealth independently or hire your own strategist.

Shape the firm's direction. Founding members receive priority access to new strategies, direct communication channels, and meaningful input on future offerings.

Limited spots available

$1MM portfolio → ~$20-30K annual coordination fees based on the 0.75%-2.5% industry standard, potentially more with account minimum fees and transaction charges.

six figures less over 10 years vs. the founding flat rate — see the Fee Drag calculator

By Year 10, you've paid over $250K+ (25%+ of initial portfolio) in cumulative fees. After 20 years, fees approach or exceed the required capital itself—a "volatility of capital" problem for financial freedom.

Standard members pay ongoing fees indefinitely. No pathway to $0 fees, regardless of financial milestones achieved.

Standard advisory service without lifetime fee lock or founding member priority. No locked-in rates, no founding member exclusive benefits, no lifetime wealth management guarantee.

Service availability subject to capacity constraints. No priority access to new strategies or input on firm direction.

The AUM headwind: a percentage of everything, every year — compounding against you.

Cumulative fees paid (the "fee mountain"). Lost compounding on AUM fees: · AUM fees pass 10% of your starting capital by .

The AUM model has one design flaw: the better you do, the more you pay.

Founding memberships are strictly limited to ensure personalized service quality and maintain white-glove execution standards. Once capacity is reached, this opportunity closes permanently—future clients will pay higher fees and miss the founding member fee lock and priority service.

Beyond capital requirements and strategy fit, we're seeking founding members who share our values and vision for a long-term partnership.

You're not looking for a transactional relationship or a quick trade. You understand that building meaningful wealth takes time, discipline, and mutual commitment. You're seeking a multi-year, potentially generational partnership where success is shared and aligned.

You value open communication, honest disclosures, and transparency over marketing hype. You appreciate that despite both the upside potential and the risk controls—nothing hidden, no fine print surprises. Trust is earned through clarity, not promises.

You understand that all investing involves risk—including possible loss of principal. You're not looking for guarantees or "sure things," but rather for a disciplined, first-principles approach backed by risk management and risk controls. You accept that targets are aspirational, not guaranteed.

You understand the "autopilot analogy": 17 years of R&D, simulation, and stress testing creates a more reliable system than blind "luck." You value rigorous methodology, documented failure modes, and detailed risk controls over decades of audited history. You recognize that every successful strategy started at the founding stage—and launching early, after the system is certified, offers asymmetric upside.

You see the value in being early. You recognize that founding-stage terms, locked-in fees, and asymmetric upside represent a unique opportunity that won't be available once the strategy scales. You're willing to partner at the ground floor in exchange for permanent advantages.

You have at least $100K in liquid investable capital (ideally $250K+), and you're seeking either pension-like cash flow or long-term wealth building. You value transparency, risk management, and complete alignment of interests over marketing promises.

We're laser-focused on wealth preservation and growth execution. Here's exactly what we do—and what we don't.

We take your existing capital ($100K+) and deploy it systematically through EPIG 500 and tax-efficient structures (whole life, etc.) to hit your 10-year wealth targets.

We manage the strategy (EPIG 500 risk controls and disciplined rebalancing) with ruthless discipline—monitoring, rebalancing, optimizing tax efficiency—so you don't have to.

We define clear wealth goals upfront (e.g., "Grow $250K to $1M by 2035"), then execute systematically with quarterly reviews to track progress and adjust strategy.

We don't create budgets, optimize cash flow, or teach basic savings discipline. We assume you've stabilized your financial life (Phase 1-2) and are ready to deploy capital (Phase 3+).

We use whole life as a wealth tool, not for insurance needs analysis. We don't draft estate documents (you need an attorney) or recommend homeowners insurance (you need an agent).

We structure strategies for maximum tax efficiency, but we don't prepare tax returns. You'll need a CPA to execute filings based on our strategy.

We're not passive portfolio managers. EPIG 500 requires active risk management and ongoing monitoring. We're hands-on strategy executors, not asset-gatherers.

Everything you need to know about Ekantik Capital Advisors and our founding member program

Learn how to begin your journey, understand the process, and know what to expect

Getting started is simple and structured:

No Obligation Consultation: Your initial consultation is completely free with no pressure or commitment required.

Schedule Free ConsultationWhat ECA Does: We partner with clients who have $100K+ in investable capital and a clear 10-year wealth goal. Our focus is wealth preservation and tax-efficient growth using EPIG 500 and strategic structures (whole life, etc.). We are NOT comprehensive financial planners—we assume you've handled cash flow stability, basic insurance, and estate documents. Our role is to deploy your capital strategically to hit your wealth targets.

For eligible investors*, Ekantik Capital Advisors offers a small flat fee per year which will remain constant until wealth goal achievement. When you achieve your 10-year wealth targets, you have the option to hire an investment strategist to continue managing your wealth independently.

Why This Matters: Unlike traditional advisors who charge fees based on assets under management (which increase as your wealth grows), our flat fee structure aligns with your goal of financial independence—not perpetual dependency.

*Eligibility Requirements: At least $100,000 in investable capital and $10,000 in risk capital

Your journey to financial freedom follows a structured 5-step process:

Comprehensive financial analysis and goal assessment to understand your current position and desired outcomes.

Personalized plan combining EPIG 500 and other tailored strategies based on your risk capital, time horizon, and freedom goals.

Execute your wealth-building strategy with expert guidance, including account setup, capital allocation, and system activation.

Ongoing optimization, performance monitoring, and quarterly reviews to ensure you stay on track toward financial freedom.

Achieve sustainable, independent wealth where your support income covers expenses with a safety margin (FCR ≥ 1.25).

Timeline: Most clients complete the full implementation within 12-14 months. The initial consultation is risk-free and allows you to fully evaluate our approach before making any commitment.

Your first year with Ekantik Capital Advisors is structured in three progressive phases designed to build trust, establish infrastructure, and deliver results:

Timeline Note: The entire process typically takes 12-14 months from first contact to full implementation. The validation phase is risk-free and allows you to fully evaluate our approach before making any commitment.

Exclusive lifetime benefits, education access, and frameworks available only to founding members

Founding members receive exclusive lifetime benefits unavailable to future clients:

Your advisory fee is locked forever — never increases, regardless of market conditions or AUM growth. Future clients will pay current market rates.

Performance-based fee reduction as you achieve financial milestones. Our goal: make you financially self-reliant so fees eventually go to zero.

Exclusive Financial Freedom Operating System — Private Skool community, live Zoom workshops, quarterly KPI reviews, and framework templates. As education evolves, you evolve.

Priority availability when capacity constraints arise. Founding members are never subject to waitlists or service limitations.

Direct advisor access with priority scheduling, faster response times, and personalized attention beyond standard service levels.

Pass to family members — Your founding benefits can be transferred to spouse, children, or designated beneficiaries.

Limited Availability: Founding memberships are strictly limited to ensure personalized service quality and maintain the exclusivity of the education community. Once capacity is reached, this opportunity closes permanently—future clients will pay higher fees and miss lifetime access to the Financial Freedom Operating System.

Understand capital requirements, passive income strategies, and wealth achievement process

Understanding capital requirements for passive income is critical for financial planning. Here's an educational comparison of different strategies to generate $100,000 in annual passive income—each with different tradeoffs in capital requirements, liquidity, and scalability:

| Strategy | Yield | Capital Needed | Scalable | Type | Liquidity | Perpetual |

|---|---|---|---|---|---|---|

| Stock Market Withdrawal | 4% | $2,500,000 | No | Passive | Yes | ~30 years |

| Dividend Income | 6% | $1,666,667 | No | Passive | Yes | No |

| Annuity | 7% | $1,428,571 | No | Passive | No | Yes |

| IUL Income | 8% | $1,250,000 | No | Passive | Yes | Yes |

| Rental Income | 8% | $1,250,000 | Yes | Semi-passive | No | May Be |

| Business Income | 30% | $333,333 | Yes | Semi-passive | No | No |

| EPIG Fund | 10% | $1,000,000 | Yes | Passive | Yes | ~30 Years |

Key Insight: A capital-efficient strategy like the EPIG Fund (10% yield, $1M capital) can require significantly less capital than traditional approaches (like 4% stock withdrawals requiring $2.5M), while offering scalability, full passivity, and liquidity. ECA specializes in implementing this capital-efficient strategy for qualified investors.

Most ECA clients arrive with investable capital already established. Our process focuses on deploying that capital through EPIG 500 and tax-efficient structures to reach agreed wealth targets within 10 years.

The Wealth Execution Cycle: This process creates a continuous improvement loop where each quarter builds on the last—setting wealth targets, deploying capital strategically, evaluating performance, optimizing allocation, and repeating. Over time, this systematic approach compounds both your wealth and your execution precision.

Learn how we're different, our philosophy, and what makes our approach unique

Ekantik Capital Advisors takes a fundamentally different approach:

Our Philosophy: Traditional advisors want you dependent forever (more AUM = more fees). ECA's goal is to make you financially self-reliant through ongoing education, proven frameworks, and community support. When you achieve true financial freedom, you can choose to hire an independent strategist or manage wealth yourself—because we've taught you how.

Take our 2-minute qualification survey to discover your best path:

Complete wealth execution system (EPIG 500 + tax strategies + education)

Long-term growth strategy for capital appreciation

Learn More

✓ No obligation • Personalized recommendations • Instant results

Compounding is a moving walkway. Every year off it must be repaid at sprint pace.

Compounding forgone on the goal while you read this page: $0

Waiting 5 years doesn’t cost 5 years. At 8%, it’s a 69% heavier annual lift.

Limited founding memberships available. Secure your lifetime benefits and begin your path to financial freedom.

First 25 members lock in lifetime benefits including:

After founding period closes: Standard members can pay six figures more over 10 years (model it in the Fee Drag calculator) and miss lifetime access to the Financial Freedom Operating System.

Pick a time that works for you — no obligation, no pressure

Your information is kept private and never shared.

Example: Plan 1 (Direct Invest) vs Plan 2 (Whole Life + EPIG)